Boosting Activation and Transaction

Value for Freo x RBL’s Co-Branded

Credit Card

Background

Over the past few years, Moneytap has grown from a credit line app to a neo bank offering products across credit line, UPI PAY (BNPL), SAVE & INVEST. Amongst 8 lenders, disbursals from RBL Bank shares ~21%

RBL Bank co-branded credit card evolved from a standard financial product to a powerful credit line and transactional tool for over 200,000 active users. With 2,000 new users joining each month, this product has unlocked new levels of user engagement.

But post application approval, card linking & transaction flow attracted nearly 300 transaction failures tickets daily where users had set their maximum transaction amount less than the what they wanted to transact, along with SIM binding failures where users had registered for the card from a number and were SIM binding with another. To top it all, RBL card users within the Freo ecosystem had their own MPIN to remember ... failing which they would have to re-link their card and go through the ordeal again.

My Role

Product designer -

User flow, prototyping,

product strategy

Team

Me :)

Arpit Bhatia, Lead Designer

Vivek Garg, PM

Senior FE Dev

Senior BE Dev

Duration

Feb’24 - Apr’24

Overview

Redesigned the onboarding and retention journey for 200,000+ existing users and 2,000+ monthly new acquisitions, achieving a 50% increase in user activation. This led to monthly transactions of ₹110 Cr ( ₹45 Cr in credit line spends, ₹50 Cr in credit card transactions,

₹15 Cr in STPL cross-selling ) and a lifetime loan book of ₹1,000+ Cr.

Challenges

The company’s vision at this point was to increase the user activation rate by 50% and monthly transaction value of the RBL Bank co-Branded Credit line led Credit card - to over 110 Cr of disbursal per month and 1000+ Cr of lifetime loan book. However, since the post-activation journey was in a SDK posed several challenges like :

⚠️

We could not predict or alter error messages to guide our users better since they came in a string format.

😮💨

Overriding on SDK UI was not possible for every screen

🤕

We could not read user’s pre-existing device settings for eg. If the user has set their

biometric or not

Apart from all of these challenges we also had to figure out a seamless card re-linking experience for our existing RBL card users post SDK deployment.

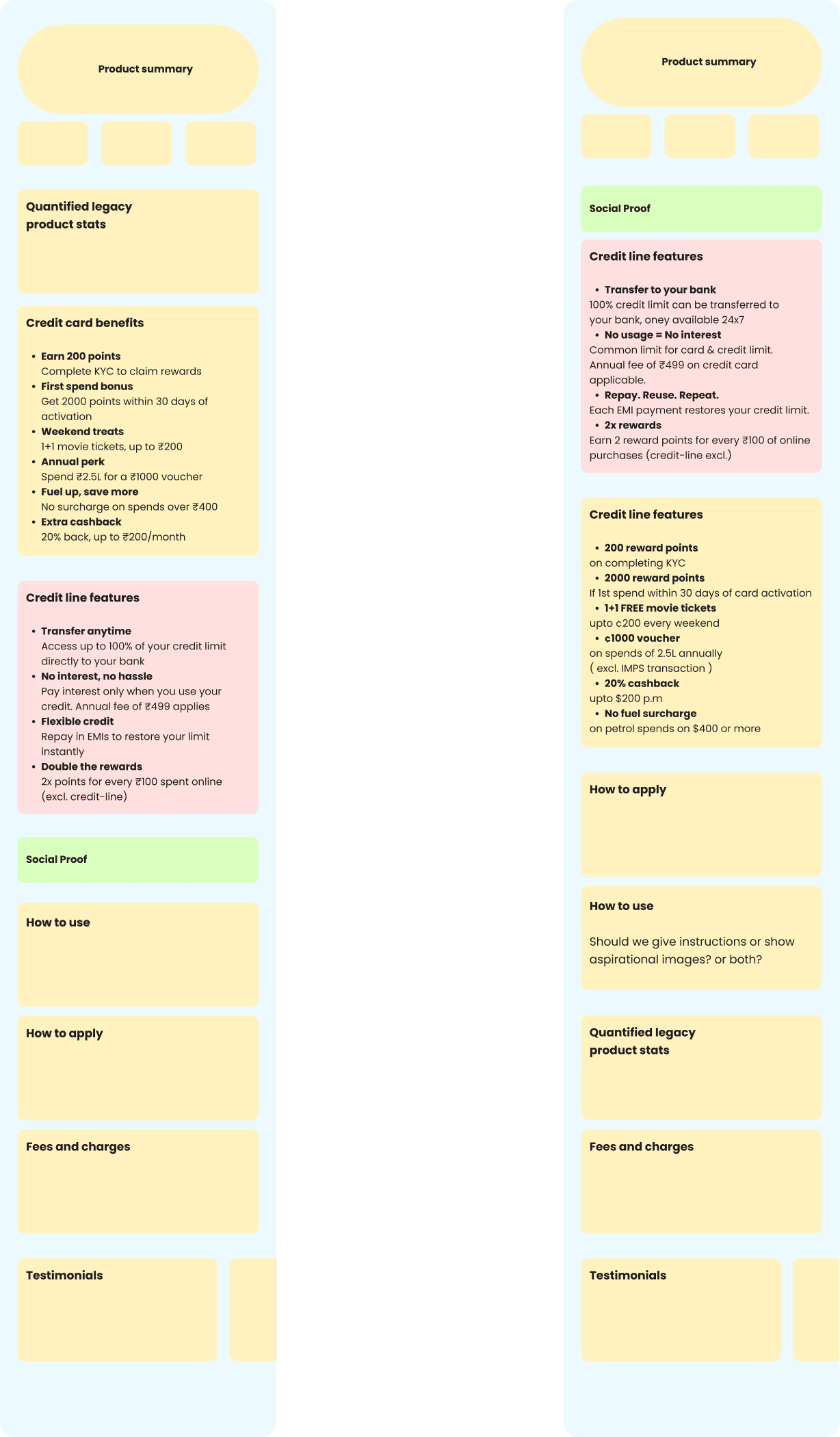

Playing around with Information Architecture

Suggested iteration

Sales

Flexible Credit: Use only what you need and pay for it your way.

Higher Limits: Handle big expenses easily with more spending power.

Easy Repayments: Choose partial payments or EMIs to stay in control.

But the question to ask here was what information do our customers value more?

How we got here

There were majorly 2 parts to this project the sales & then the activation of the line by linking your credit card to start transferring money.

Freo x RBL Bank Credit Card is a legacy product so over time it had a lot of offerings. Hence it was even more crucial now to decide how we wanted to present it.

Research Insights

Our customer success & collections team helped us with a market research to understand user perceptions, adoption and usage of RBL Bank co-branded credit card

~71%

users didn't understand the importance of editing Card Transaction Limits

~36%

We could not read user’s pre-existing device settings for eg. If the user has set their

biometric or not

~28%

face confusion with dual SIM phones

(unclear which SIM to use)

~42%

Re-asking for biometric permission confused users and required clear justification

Card Verification

Receiving or approving credit as an eco-system is large and is a 90% rejection process.

In this case study we are talking about card activation and card transactions but here is a macro view of the process.

One of the main challenges were :

• User data won’t be saved in case of loss of signal etc. and the user will need to restart their journey.

• User needs to complete steps until setting MPIN for their card to be activated.

So we thought

Could we rearrange the steps where SIM Binding is done before entering the SDK?

While that wasn’t possible, at least we tried!

😅

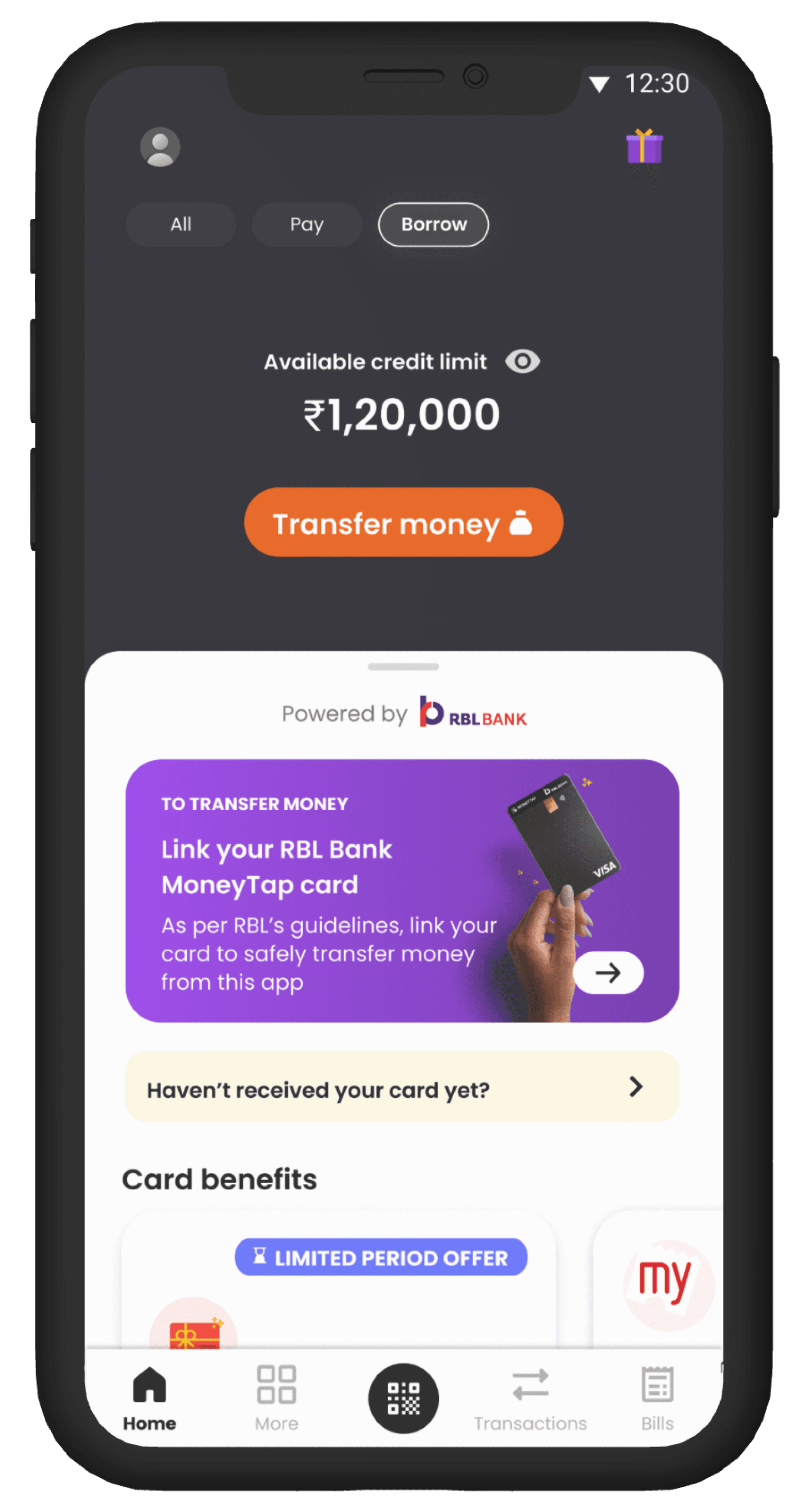

Users could start the journey from multiple intents & entry point for eg. to transact money, to check their credit limit or to link their card. To accommodate this I designed variations of these entry points.

This space was also created to promote offer and cross - sell other products for future

While card verification screen was fairly simple we still ended up multiple iterations of it. Questions like is Freo verifying these details or RBL? Can we auto-detect the registered mobile no. with card? What is the user hasn’t received the card yet?

Left to Right - stakeholder feedback :

Can we create a common credit card verification screen where changing the bank icon changes the application form?

We can’t retrieve mobile no. linked to the card, before SIM verification step. visibility for edge case should be present before entering the form.

Following Jacob’s Law I simplified the screen even further.

SIM Binding

When it came to SIM Binding an array of questions came up like :

Can we provide real-time feedback if the wrong SIM is used during verification?

What happens if users are on dual-SIM phones or have recently switched SIMs?

How do we handle users who don’t have their primary registered number on the device?

No SIM found

Incorrect SIM

No SMS balance / Network

Setting MPIN / Biometric & usage schema

for setting biometric we had some questions like :

• Can we read if the user had set biometric on their device?

• What if user’s don’t give biometric permission, will they be able to set it later?

Answering a common questions of users regarding when they are setting PINS.

Incorrect MPIN inline errors were coming in string format so we simply couldn’t edit those texts. But what we could do is intercept and have an overlay UI to provide better messaging, reducing reliance on SDK errors.

While re-entering the RBL SDK, we wanted to still nudge users who did not set biometric earlier to do to decrease cognitive load in future interactions.

Device Biometric permission ✅

App biometric set ✅

Device Biometric permission ✅

App biometric set ❌

Device Biometric permission ❌

App biometric set ❌

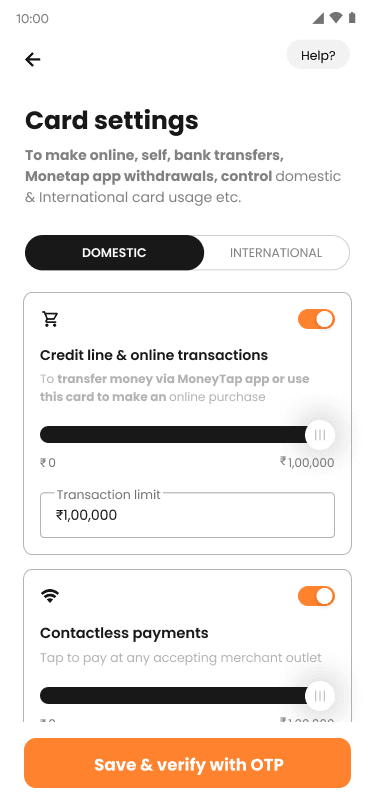

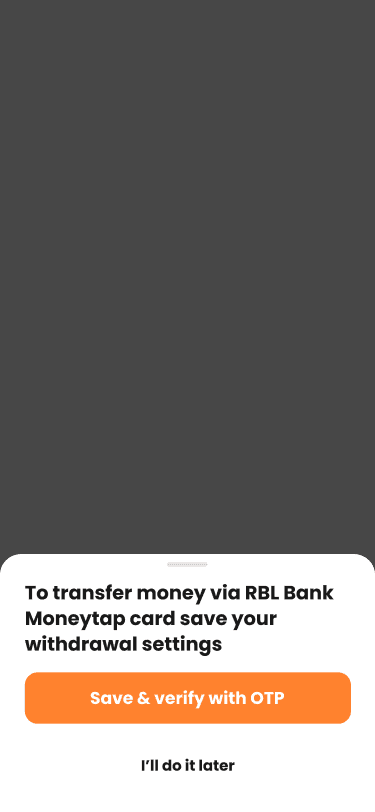

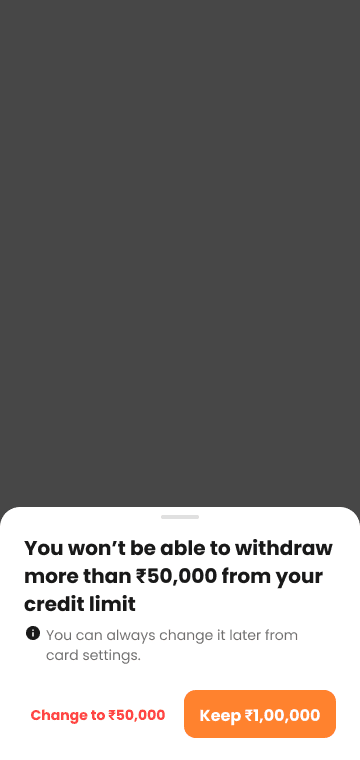

Card settings

We were facing a major challenge at this step which resulted in 300 IMPS transaction failures customer success tickets in a day!!! When users came they quickly hit the verification CTA and moved ahead, often missing to set their maximum transaction value.

Conducted a quick MOM test around the office campus with 8 participants and here is what I found out :

Old design

Iteration 1

👍🏽

People understood the purpose of the page and the product it belonged to

🧐

People asked “Is this limit my monthly transaction limit?”

🤕

The switch between Domestic &

International card settings was not clear

☹️

People inquired “If my limit is 1 Lakh, does decreasing amount here reflect the same on my credit limit?”

Iteration 2 post usability test

🎊 Impact 🎊

300 to 70

Customer

Success Tickets/_day

38%

Monthly transaction value/_user

64%

Card Activations within

3 days of receiving card

70%

Card re-linking attempts